![]()

Second Hand News

Submitted by Grunden Financial Advisory, Inc on March 3rd, 2010Disclosure: Every investor’s situation is different and investment decisions are best made within the context of a financial plan. Consult your professional advisor. Comments reflect our opinion only and not intended for financial advice.

Jim Parker, a Vice President at DFA Australia Limited, shares his thoughts on how reporting done by the media can sometimes distract investors who want to build long-term wealth.

Second Hand News

By Jim Parker

Vice President, DFA Australia Limited

Trying to understand financial markets by tracking the daily media headlines is like trying to tell the time by tracking the second hand of a watch. By focusing on the minutiae, you risk missing the big picture.

Much of the investment-related news that fills the vast gaps between the advertisements in the day-by-day world of the media is undoubtedly fascinating, particularly to those who live their lives that way.

But a lot of it really is a distraction for those who want to build long-term wealth through investment. That's because while the news story keeps changing according to the events of the hour or the day, the story of sound investment doesn't change much at all.

This story says the best approach is to work with markets, not against them; structure portfolios around risks that are related to return, diversify across and within asset classes, pay heed to costs and taxes, remain disciplined and rebalance as your own needs and circumstances change.

Discipline amid the media and market noise is important because while there is a long-term return from risking your capital, the return is not there every year. Returns over shorter time periods are random and unpredictable.

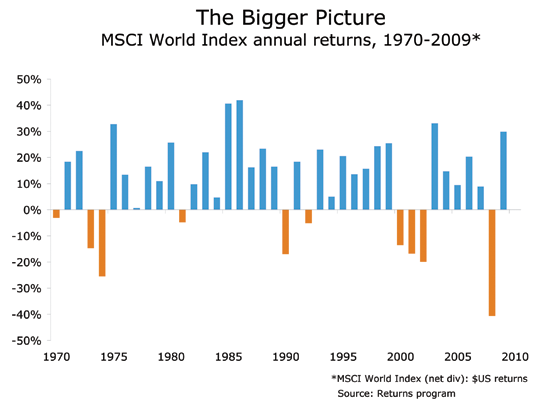

Take a look at this chart, showing the annual returns for the past 40 years of global share markets, as measured by the MSCI World Index. You can see that some of the best years (1975, 2003 and 2009) came straight after some of the worst (1973-74, 2000-02 and 2008).

Of course, getting the timing right around these turning points is the holy grail of investing. Trouble is no-one has been able to show yet that they can perform this feat with any consistency. Getting out before the peak is one thing, getting back in without missing the rebound is another.

The better approach is to stay invested, although this doesn't preclude rebalancing occasionally away from risky assets if your retirement goals are on track. The difference is that this decision is made according to your own situation, not what is happening in the markets at a particular time.

The difficulty of market timing was highlighted by a recent Morningstar study[1] which looked back on the past decade (2000-2009) to assess the average return of the US mutual funds it rates and compared them with the return actually received in that time by the average investor.

The results make for sobering reading. While the annualized return for the average fund in this period was 3.18%, the average investor received just 1.68% or around half of the fund total. In US equities, the average investor earned a mere 0.22% annualized compared with 1.59% for the average fund.

The reasons for this disparity are depressingly familiar. People succumbed to the old twin devils of greed and fear, loading up on risk out of proportion to their needs during the good times and dumping risk altogether in the bad.

And they did this usually because they were focused too much on short-term returns, the daily noise, the froth and bubble — the second-hand news.